By calculating the present value, you can understand the effective cost in today’s dollars, potentially helping you with budgeting or financial planning. If you own an annuity, the present value represents the cash you’d get if you cashed out early, before any fees, penalties or taxes are taken out. You can usually find the current present value of your annuity on your policy statements or your online account. The future value should be worth more than the present value since it’s earning interest and growing over time. We specialize in helping you compare rates and terms for various types of annuities from all major companies.

Present Value Spreadsheet Calculations

When you set all the required parameters, you will immediately see the results summarized in a table. You can also follow the progress of your annuity balance in a dynamic chart and annuity table of the payment schedule. If you would accountant partners payroll and hr software like to learn more about annuities, check our time value of money calculator or the annuity payout calculator. Using the previous inputs, fill in the interest rate of 0.05, the time period of 3 (years), and payments of -100.

Would you prefer to work with a financial professional remotely or in-person?

You can also use this online calculator to double-check your calculations for the PV of an ordinary annuity. You can find the PV of an ordinary annuity with any calculator that has an exponential function, even regular (non-financial) calculators. You can use a financial calculator or a spreadsheet application to more efficiently calculate present values. A common variation of present value problems involves calculating the annuity payment.

Present Value of a Perpetuity (t → ∞) and Continuous Compounding (m → ∞)

A portion of the payments always goes toward the interest that is being charged on the loan. The best way to demonstrate the strengths of the annuity calculator is to take some annuity examples. If you’re looking for an investment strategy that goes beyond “buy and hold” while controlling risk and requiring as little as 30 minutes a month to manage, this is the answer. Take back control of your portfolio and start getting results today.

The present value is handy to know if you want to compare the windfall from selling an annuity against its expected payments in the future. The future value lets you know what your account will be worth after a period of contributions and growth before annuitization. Keep reading to learn how to calculate each value and how to use this knowledge to secure your future.

The present value of annuity table contains the factors used to determine an individual cash flow at one point in time. This can be done by discounting each cash flow back at a given rate by using various financial tools, including tables and calculators. With a fixed annuity, your contributions grow at an interest rate set by the insurance company.

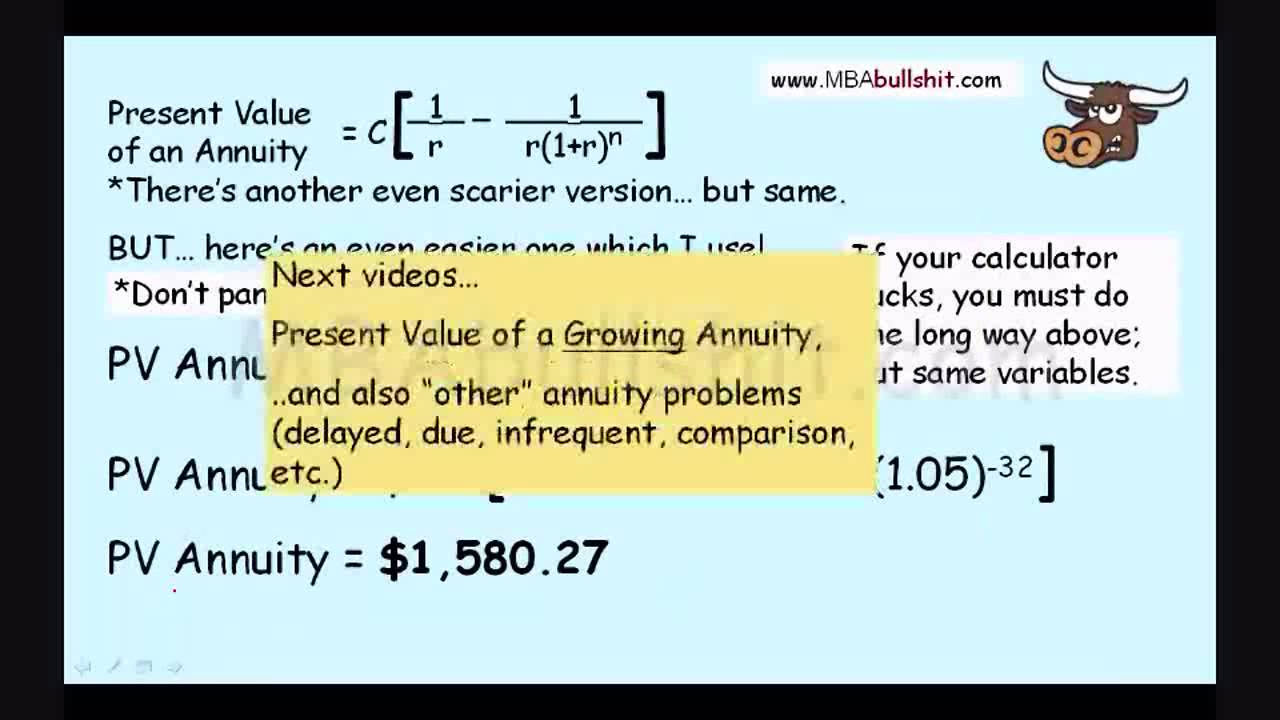

Additionally, you can use a spreadsheet application such as Excel and its built-in financial formulas. An annuity table is a tool for determining the present value of an annuity or other structured series of payments. To determine an individual cash flow, or annuity factor, by using this table, you would look across the top row for the number of periods and down the left side for the interest (or discount) rate. Entering these values in an equation yields the present value of an annuity.

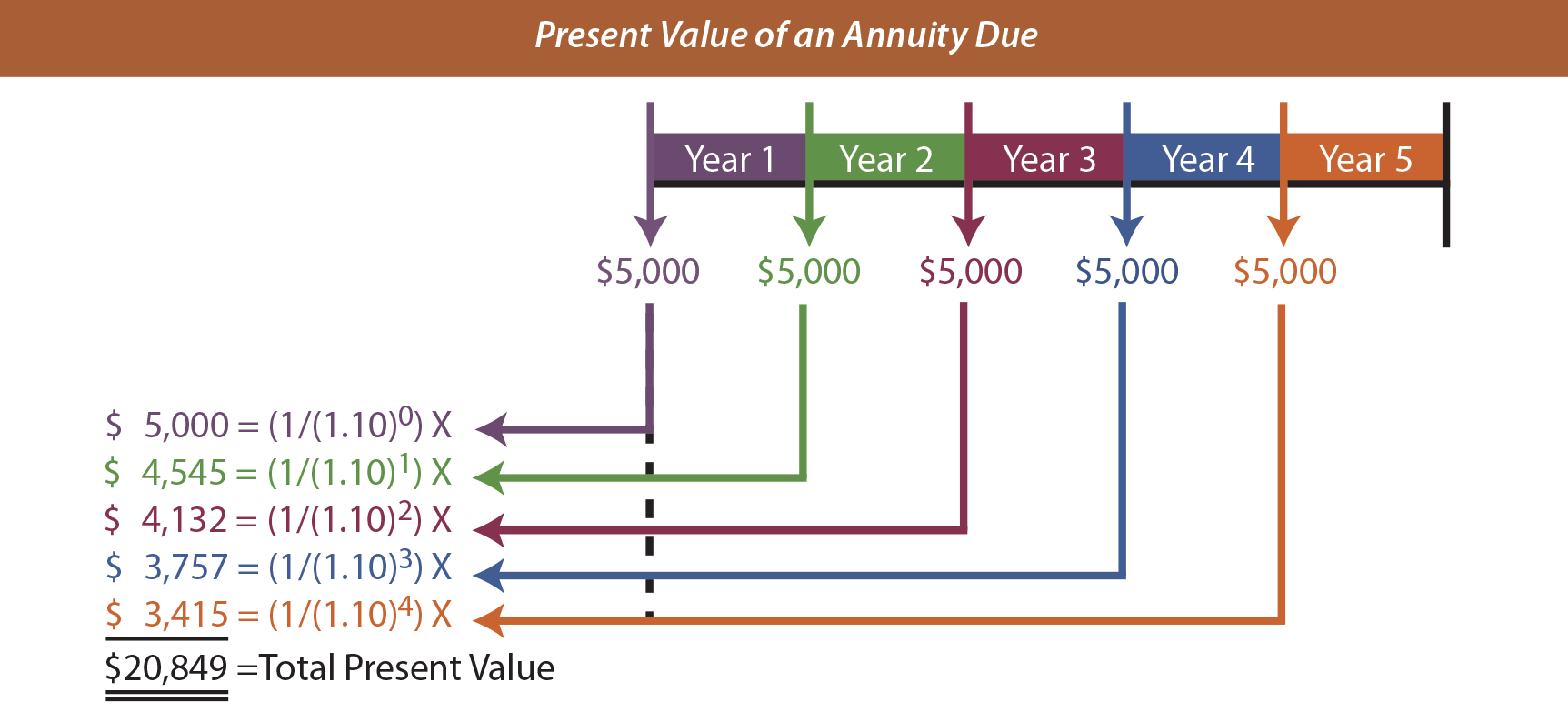

- The present value of an annuity is the amount of money needed today to cover future annuity payments.

- When calculating the present value (PV) of an annuity, one factor to consider is the timing of the payment.

- A lower discount rate results in a higher present value, while a higher discount rate results in a lower present value.

- As long as we know two of the three variables, we can solve for the third.

This variance in when the payments are made results in different present and future value calculations. For example, if an individual could earn a 5% return by investing in a high-quality corporate bond, they might use a 5% discount rate when calculating the present value of an annuity. The smallest discount rate used in these calculations is the risk-free rate of return. Treasury bonds are generally considered to be the closest thing to a risk-free investment, so their return is often used for this purpose. To complicate matters further, the last payment amount may be unknown and incalculable, particularly if interest rates are variable. You can’t calculate a present value from an unknown number nor can you use an annuity formula where a payment is in a different amount.

In the rare circumstance where the final payment is exactly equal to all other annuity payments, you can arrive at the balance owing through a present value annuity calculation. In this instance, since you are starting at the end of the loan, the future value is always zero, so to bring all payments back to the focal date you only need Formula 11.4. To determine accurately the balance owing on any loan at any point in time, always start with the loan’s starting principal and then deduct the payments made. This means a future value calculation using the loan’s interest rate. What’s more, you can analyze the result by following the progress of balances in the dynamic chart or the annuity table.

For example, you can use it either for regular deposits or withdrawals, for multiple frequencies, or you can compare ordinary annuity vs. annuity due. Having $10,000 today is better than being given $1,000 per year for the next 10 years because the sum could be invested and earn interest over that decade. At the end of the 10-year period, the $10,000 lump sum would be worth more than the sum of the annual payments, even if invested at the same interest rate. An individual cash flow or annuity can be determined by discounting each cash flow back at a given rate using various financial tools, including tables and calculators.

Leave a Reply